Getting hurt in a car accident is overwhelming enough on its own. Then the bills start arriving. This medical bills after car accident guide exists because most people have no idea how the payment system works, which insurers pay first, or what to do when multiple providers all want money at the same time. The formal term attorneys and insurers use is "medical expense recovery," and knowing how it actually works can protect your finances and strengthen your claim. The average bodily injury claim has jumped 81% since 2016, now reaching $29,400. The stakes are real.

Table of Contents

- Key Takeaways

- Understanding car accident medical expenses

- The payment hierarchy you need to know

- How to manage your bills step by step

- Common mistakes and negotiation strategies

- What to expect after submitting your medical claims

- My take on navigating this process

- You do not have to figure this out alone

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Bills arrive in waves | Medical expenses from different providers trickle in over months, requiring organized tracking from day one. |

| MedPay and PIP pay first | These coverages activate immediately after a crash, before health insurance or the at-fault driver's policy. |

| At-fault insurance pays last | The other driver's liability insurance only pays out at settlement, not during your treatment. |

| Medical liens can be negotiated | Providers frequently accept 30 to 50% less than billed amounts rather than risk receiving nothing. |

| Deadlines are unforgiving | Missing treatment windows in no-fault states can permanently eliminate your PIP benefits. |

Understanding car accident medical expenses

Car accident costs rarely arrive as one clean bill. They come in layers, and the total is almost always higher than victims expect. A single emergency room visit for a high-complexity case can cost between $1,500 and $10,000, and that is before the radiologist, the attending physician, or the specialist all send separate invoices for the same visit.

Here is what a typical injury generates in medical paperwork:

- Emergency room visit — facility fee plus separate physician charges

- Ambulance transport — often $400 to $1,200 per ride, frequently not covered at in-network rates

- Imaging — MRIs and CT scans run $1,000 to $3,000 each

- Surgery — costs vary wildly by procedure and can reach six figures

- Physical therapy — ongoing sessions over weeks or months

- Prescription medications — co-pays and out-of-pocket costs add up faster than expected

- Medical supplies — braces, crutches, and home care items

- Mental health treatment — often overlooked but fully recoverable, including anxiety and PTSD treatment following a crash

Bills from different providers arrive on completely different schedules. Your hospital sends one in week two. Physical therapy bills come monthly. The radiologist may not send anything for three months. Medical bills arrive in staggered waves over many months, which means you cannot simply wait for a stack of paperwork to appear. You need a system from the beginning.

Pro Tip: Keep a dedicated accordion folder or digital folder labeled by date. Every explanation of benefits, every billing statement, and every receipt goes in there. This becomes your financial evidence file.

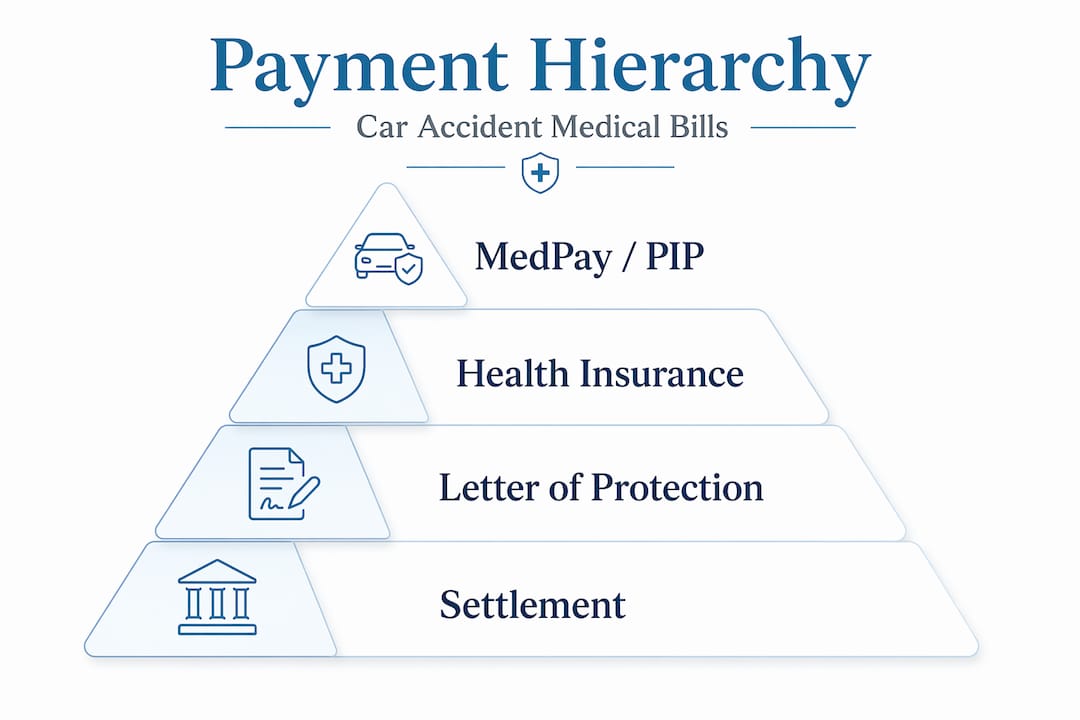

The payment hierarchy you need to know

This is the single biggest source of confusion for accident survivors. Paying medical bills after accident cases is not random. There is a specific order, and understanding it changes everything about how you respond to bills as they arrive.

Here is how the payment sources stack up:

| Payment Source | Timing | Key Details |

|---|---|---|

| MedPay / PIP | 0 to 30 days | Pays regardless of fault; MedPay limits range from $1,000 to $50,000 |

| Private health insurance | 1 to 6 months | Pays after MedPay/PIP is exhausted; carries subrogation rights |

| Medical liens / Letters of Protection | Ongoing during treatment | Providers treat now, get paid from settlement later |

| At-fault driver's liability insurance | 6 months to 3+ years | Pays only at claim settlement, not during treatment |

Medical Payments coverage (MedPay) and Personal Injury Protection (PIP) are your immediate resources. PIP is mandatory in no-fault states like Florida, Michigan, and New York. MedPay is optional in most states but covers medical costs for you and passengers quickly, regardless of who caused the crash.

Health insurance steps in after those limits are exhausted. The catch is subrogation. Your health insurer pays your bills and then has a legal right to be reimbursed from your settlement. That repayment obligation does not disappear just because you settle with the at-fault driver.

In states where MedPay and PIP limits run out quickly, a Letter of Protection (LOP) becomes critical. This is a written agreement between your attorney and your medical provider stating that bills will be paid from your future settlement. It allows you to continue receiving care without paying out of pocket while your case is pending.

Pro Tip: If you live in a no-fault state, get to a doctor within 14 days of your accident. Missing that window can permanently forfeit your PIP benefits, even if your injuries are legitimate.

How to manage your bills step by step

Organization is what separates people who recover their full costs from those who leave money on the table. The steps below cover what you need to do from the day of the crash through the final settlement.

-

Document everything at the scene. Photograph injuries, take the police report number, and record the other driver's insurance information. Your first 24 hours after the crash set the foundation for your entire claim.

-

Seek medical care immediately. Even if you feel fine, certain injuries like whiplash and traumatic brain injuries do not present symptoms for days. Getting examined creates a timestamped medical record directly linking any injuries to the accident.

-

Notify all of your insurers. Contact your own auto insurer to activate MedPay or PIP. Notify your health insurer as well. Do not wait for bills to arrive before making these calls.

-

Start a symptom diary. Write down daily pain levels, limitations, emotional distress, and how your injuries affect work and daily life. Linking injuries to the crash through consistent documentation is far more persuasive to adjusters than a vague injury summary.

-

Track every bill and payment. Log the provider name, service date, billed amount, amount paid by insurance, and your remaining balance. A simple spreadsheet works. What matters is consistency.

-

Communicate with providers about payment. If a bill arrives before your claim is resolved, call the provider's billing department. Many providers will place your account in a "hold" status or accept a lien arrangement when they know an attorney is involved.

-

Avoid treatment gaps. Stopping treatment and restarting looks suspicious to insurance adjusters. They will argue your injuries healed and then were aggravated by something else. Consistent care protects both your health and your claim.

Pro Tip: Request itemized bills from every provider, not summary statements. Itemized bills allow you or your attorney to identify billing errors and disputed charges before they become part of your claim.

Common mistakes and negotiation strategies

One of the most expensive misconceptions in car accident cases is the belief that the other driver's insurance will cover your bills as they arrive. It does not work that way. The at-fault driver's liability insurance covers medical costs only after the entire claim concludes. That can take years. Understanding car accident costs means accepting that you need interim coverage in place from day one.

Here is where many survivors go wrong and what to do instead:

- Ignoring subrogation. If your health insurer paid $15,000 in bills and you settle for $30,000, that insurer expects repayment. Health insurance subrogation can dramatically reduce what you actually pocket. An experienced attorney can often negotiate that subrogation lien down significantly.

- Accepting the first settlement offer. Initial offers rarely account for future medical costs, ongoing therapy, or long-term complications. Accepting early can leave you personally responsible for bills that arrive months later.

- Missing deadlines in no-fault states. The 14-day PIP window is not a suggestion. Crossing that deadline means losing access to benefits you paid for through your own premiums.

- Not negotiating medical liens. Medical providers negotiate liens regularly. Liens can be reduced 30 to 50% during settlement because providers prefer a guaranteed lower payment over the risk of collecting nothing.

- Underinsured or uninsured drivers. If the at-fault driver carries minimal coverage or none at all, your own Uninsured Motorist (UM) or Underinsured Motorist (UIM) coverage becomes your primary recovery option. Review your own policy carefully. Understanding your legal rights after an accident helps you use every coverage layer available.

What to expect after submitting your medical claims

Once your treatment is complete or your condition has stabilized, your attorney (or you, if unrepresented) will compile all medical records, bills, and supporting documentation into a demand package. That package goes to the at-fault driver's insurer, and the negotiation process begins.

Here is a general timeline and payment distribution:

| Stage | Typical Timeframe | What Happens |

|---|---|---|

| Active treatment | 0 to 18 months | MedPay, PIP, health insurance, and liens cover ongoing costs |

| Demand submitted | After treatment stabilizes | Attorney sends full claim package to liability insurer |

| Negotiation and settlement | 6 months to 3+ years total | Insurer reviews, counters, and parties negotiate |

| Settlement distribution | Within 30 days of agreement | Attorney fees paid first, then medical liens and subrogation, then remainder to you |

Future medical costs also factor in. If your doctor determines you will need ongoing treatment, surgery, or long-term care, those projected costs should be included in your demand. Settling before you know the full picture of your medical future is one of the most common and costly mistakes accident survivors make. If your case is in Pennsylvania, the state-specific rules around medical expenses and insurance affect your options in ways that a national overview cannot fully capture.

My take on navigating this process

I have talked with hundreds of accident survivors, and the pattern I see repeatedly is this: people assume the system will sort itself out. They expect their insurer or the other driver's insurer to manage everything and send them a check when it is done. That is not how it works, and the cost of that assumption is enormous.

What I have learned is that meticulous documentation from day one is worth more than any single piece of legal advice. The survivors who come out whole are the ones keeping symptom diaries, saving every bill, and calling their insurer the same week as the crash. Not the same month. The same week.

The subrogation issue surprises almost everyone. You get a settlement check and feel relieved, only to learn that a significant portion is already spoken for by a lien you did not fully account for. I have seen that reduce a $50,000 settlement to a $20,000 payout after fees and liens. The good news is that liens are negotiable, and an attorney who handles car accident cases regularly knows exactly how to push back.

My strongest advice: consult an attorney before you speak with any insurance adjuster, including your own. Many personal injury attorneys offer free consultations. The consultation costs nothing. Talking to an adjuster without understanding your rights can cost you everything.

— Scott

You do not have to figure this out alone

Managing accident injury medical bills while you are recovering physically and emotionally is genuinely hard. Accidentsurvivalguide was built by Scott Tischler and Kathy Carr specifically because they lived through this process and knew there had to be a better way to help survivors understand their options.

At Accidentsurvivalguide, you will find free guides on documentation, insurance tactics, lost wages, pain and suffering, and your legal rights. Whether you are dealing with a crash in Massachusetts or trying to understand how the payment process works nationwide, the resources are free and built for real people, not lawyers. Visit Accidentsurvivalguide.com to access the full library and connect with experienced legal professionals who can help you protect your recovery.

FAQ

Who pays my medical bills right after a car accident?

MedPay or PIP insurance pays first, typically within the first 30 days, regardless of fault. Your private health insurance covers remaining costs after those limits are exhausted.

How long does it take to get medical bills paid after an accident?

Full payment through the at-fault driver's liability insurance happens only after settlement, which can take anywhere from six months to three years or more depending on case complexity.

Can I negotiate my medical bills from a car accident?

Yes. Medical liens are regularly negotiated during settlement, and providers often accept 30 to 50% reductions because they prefer a guaranteed payment over an uncertain one.

What happens if the at-fault driver has no insurance?

Your own Uninsured Motorist (UM) coverage becomes the primary recovery source. Review your own auto policy to understand your UM and UIM limits before assuming you have no options.

Does health insurance have to be paid back from my settlement?

In most cases, yes. This is called subrogation. Your health insurer has a legal right to recover what it paid from your settlement proceeds, though an attorney can often negotiate that amount down significantly.