If you just got in a car accident and someone mentioned personal injury protection, you may have assumed it covers every medical bill and expense you now face. It does not, and that assumption costs accident victims thousands of dollars every year. The role of personal injury protection explained simply: it is a no-fault auto insurance coverage, formally known as PIP, that pays for your medical expenses, lost wages, and related costs regardless of who caused the crash. Understanding exactly what PIP does and does not do is one of the most practical steps you can take right now.

Table of Contents

- Key takeaways

- The role of personal injury protection explained

- State-specific rules that change everything

- Filing a PIP claim after an accident

- Financial gaps PIP cannot fill

- My perspective on navigating PIP claims

- Get help navigating your accident recovery

- FAQ

Key takeaways

| Point | Details |

|---|---|

| PIP is no-fault coverage | Your own insurer pays your benefits regardless of who caused the accident, speeding up access to care. |

| State rules vary significantly | Benefit caps, treatment deadlines, and mandatory minimums differ by state and directly affect your payout. |

| Timing is everything | Missing initial treatment windows, like Florida's 14-day rule, can permanently disqualify your PIP claim. |

| PIP does not cover everything | Property damage and third-party liability fall outside PIP scope, creating potential financial gaps. |

| Deadlines can cost you benefits | States like Michigan require filing within one year or you forfeit wage-loss and medical benefits entirely. |

The role of personal injury protection explained

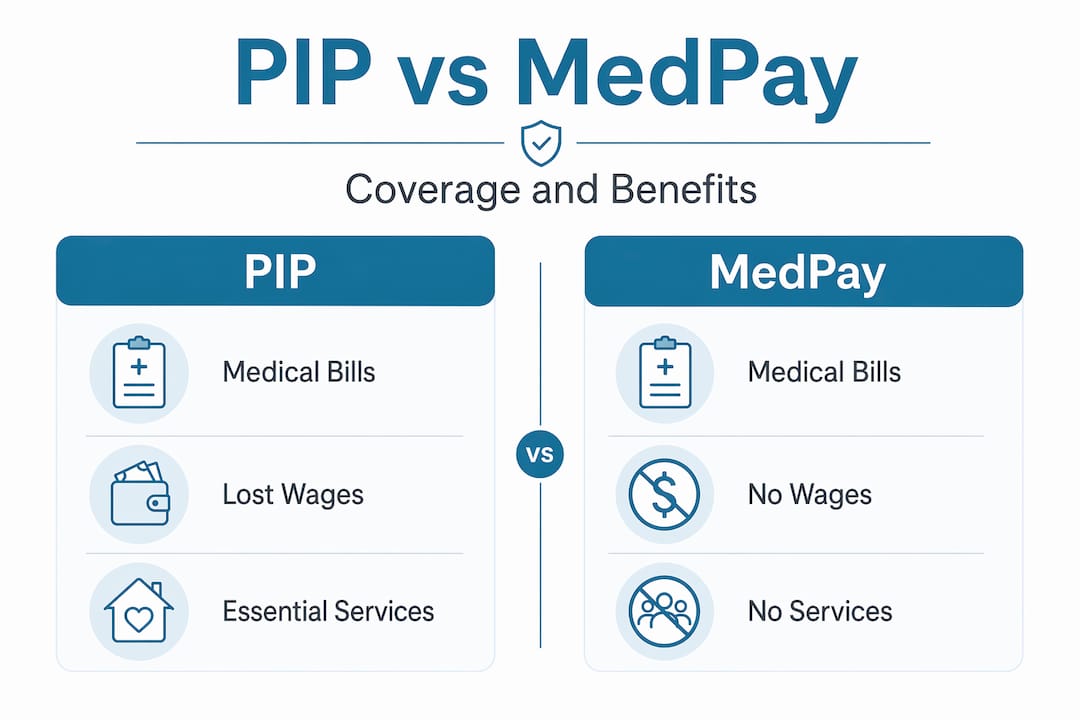

PIP insurance, often called no-fault insurance, is first-party coverage. That means you file a claim with your own auto insurer, not with the at-fault driver's insurance company. PIP pays accident-related medical expenses and related costs regardless of fault, and it does not cover property damage. That distinction matters more than most people realize.

Here is what PIP typically covers:

- Medical bills: Hospital visits, surgeries, rehabilitation, and follow-up care

- Lost wages: A portion of income you cannot earn while recovering

- Essential services: Costs for tasks you cannot perform due to injuries, like childcare or housekeeping

- Funeral expenses: Death benefits for fatal accidents

What PIP does not cover is equally important to understand. Property damage to your car, injuries to other drivers or passengers in other vehicles, and any third-party liability claims all fall outside PIP's scope. Those are handled through collision coverage and liability insurance.

Pro Tip: Think of PIP as your personal recovery fund, separate from any legal dispute over fault. Use it to keep medical bills paid while the liability question gets sorted out.

PIP differs from MedPay, another medical coverage option, in one key way. MedPay covers medical bills only, while PIP extends to lost wages and essential services. Liability insurance, by contrast, covers injuries and damages you cause to others. They serve different functions and are not interchangeable.

PIP is mandatory in about a dozen states and optional in others. In states without a no-fault system, drivers rely on liability insurance and health insurance instead. Knowing whether your state requires PIP and at what minimum level shapes everything about your financial recovery after a crash.

| Coverage type | Who it protects | Fault required? |

|---|---|---|

| PIP | You and your passengers | No |

| Liability insurance | Other parties you injure | Yes |

| MedPay | You and your passengers | No |

| Health insurance | You | No |

State-specific rules that change everything

Understanding personal injury protection at a national level only goes so far. The specific rules in your state will determine how much you actually receive and when.

Florida offers one of the most referenced examples. Florida PIP requires $10,000 minimum coverage, with medical benefits reimbursed at 80% and disability benefits at 60%, plus a $5,000 death benefit. That sounds straightforward until you realize the cap is shared across all benefit categories. One surgery can exhaust it fast.

Florida also enforces a strict treatment deadline. Missing initial care within 14 days disqualifies you from PIP benefits entirely, with no exceptions. Not feeling badly injured is not a valid excuse in the eyes of the insurer. Many people skip the ER because they feel fine, then discover days later that their injuries are real and their claim window has closed.

There is one more Florida-specific detail that surprises accident victims. The designation of an emergency medical condition (EMC) by a qualifying provider affects your benefit ceiling. Without an EMC designation, your available medical benefits may be capped at $2,500 instead of the full $10,000.

New Jersey takes a different approach. New Jersey requires $15,000 minimum PIP coverage per person per accident, covering medical costs, income continuation, essential services, and death benefits. Drivers in New Jersey can also elect whether PIP is primary or secondary depending on whether they carry health insurance.

Michigan operates under a broader no-fault framework. Michigan PIP covers medical bills and wage loss regardless of fault, and reimburses 85% of lost wages for up to three years. That is among the most generous wage-loss coverage in the country. However, see what to do after an accident in Michigan's no-fault system because specific filing steps apply.

- Know your state's minimum PIP limit before an accident, not after

- Confirm whether your state uses primary or secondary PIP relative to health insurance

- Find out whether your state has treatment deadlines that trigger eligibility

- Understand if your state uses EMC or similar designations that cap benefits

- Identify your filing deadline for wage-loss claims

Pro Tip: Call your insurance agent today and ask specifically: "What is my PIP limit, when does coverage begin, and are there any treatment windows I need to know about?" Most agents will not volunteer this information unprompted.

Filing a PIP claim after an accident

PIP's no-fault structure allows fast access to benefits without waiting for a liability decision. That speed advantage evaporates quickly if you do not act promptly. Here is how to protect your claim from the start.

Seek medical care immediately. Do not wait to see if symptoms develop. Go to the ER, an urgent care facility, or your doctor the same day if possible. This is both medically sound and legally critical. Missing procedural deadlines can cause claim denial or suspension of PIP benefits, and there is rarely a way to recover once the window closes.

Notify your insurer right away. Call your auto insurance company the same day or the next business day. Ask for the PIP claims department specifically. Get a claim number in writing.

Gather your documentation. Your insurer will require specific items to process the claim:

- A copy of the police report and accident details

- All medical records and bills from treating providers

- Proof of employment and lost wages, such as pay stubs or a letter from your employer

- Receipts for essential services you paid for due to your injuries

Understand independent medical exams (IMEs). Your insurer has the right to request an IME, where a doctor they select evaluates you. IMEs can affect your ongoing PIP eligibility. Attend every scheduled IME and bring copies of all your medical records. Skipping one gives your insurer grounds to suspend your benefits immediately.

Watch filing deadlines with the same urgency as treatment deadlines. In Michigan, filing a PIP application within one year is mandatory. Miss it and you can lose both medical and wage-loss benefits permanently. Other states have similar cutoffs.

Understanding how to avoid costly insurance claim mistakes can be the difference between a full recovery and a financial crisis.

Financial gaps PIP cannot fill

This is where many accident victims get blindsided. PIP coverage has real financial limits and understanding personal injury protection means acknowledging those limits honestly.

The core problem is the shared cap. In Florida, that $10,000 limit must cover medical bills, disability payments, essential services, and death benefits across one policy period. PIP benefits exhaust faster than expected due to these formula-based limits and category sharing. A single MRI and two weeks of physical therapy can consume a significant portion of the cap before wage-loss benefits even kick in.

Here is what you should plan for once PIP is exhausted:

- Health insurance picks up secondary costs if you have it and if your policy allows coordination with auto claims

- Liability claims against the at-fault driver can recover costs beyond PIP limits, but those take time

- Underinsured or uninsured motorist coverage fills gaps when the other driver carries inadequate insurance

- Out-of-pocket costs may still apply depending on your health insurance deductible and co-pay structure

PIP interacts with health insurance and liability claims, requiring careful coordination to minimize what you pay out of pocket. Which coverage pays first affects timing and your subrogation rights, meaning your health insurer may seek reimbursement from your settlement later.

| Financial source | Covers after PIP is exhausted | Timing |

|---|---|---|

| Health insurance | Medical bills (minus deductible) | Immediate, secondary |

| Liability claim | All damages against at-fault party | Months or longer |

| Underinsured motorist coverage | Gap between other driver's limit and your damages | After liability resolved |

| Out-of-pocket | Whatever remains | Ongoing |

Supplemental accident insurance or umbrella policies can provide an additional financial buffer. They are worth reviewing before a crash happens, not after.

My perspective on navigating PIP claims

I have seen firsthand how quickly the promises of PIP coverage can fall apart when accident victims make what seem like small, reasonable decisions. Taking a day to see how you feel before going to the doctor. Assuming your insurer will guide you through the process. These are understandable choices that can permanently close the door on benefits you paid for.

What I have learned is that the insurance system is not designed to remind you of your deadlines. The 14-day treatment rule in Florida is a perfect example. Early care is crucial for preserving benefits, yet the rule is buried in policy language most people never read before an accident.

The other thing I have seen create real problems is assuming PIP will cover everything and skipping a conversation with a personal injury attorney. Once PIP limits are exhausted or disputed, you are dealing with a legal process whether you want to be or not. Getting early advice, even a free consultation, gives you a clear picture of where you stand before the bills pile up.

My honest take: treat every PIP claim as if the deadline was yesterday. Document everything, go to the doctor immediately, and do not let an IME catch you unprepared. The accident was not your fault. Getting cut off from benefits because of a procedural mistake would be.

— Scott

Get help navigating your accident recovery

If you are dealing with insurance questions after a crash, you do not have to figure it out alone. Accidentsurvivalguide was built specifically for this moment.

Accidentsurvivalguide provides free, state-specific resources covering everything from medical documentation to insurance company tactics, so you know what to do and what to avoid. The guides at Accident Survival Guide walk you through each step of the process, whether you are filing a first PIP claim, facing a benefit dispute, or wondering what happens when coverage runs out. Readers in states like Virginia can also find tailored recovery guidance for their specific laws and claim rules. Do not accept a low offer or miss a deadline because you did not know your options.

FAQ

What does personal injury protection actually cover?

PIP covers medical bills, a portion of lost wages, essential services, and funeral costs after a car accident, regardless of fault. It does not cover property damage or injuries to other drivers.

Is personal injury protection required in every state?

No. PIP is mandatory in roughly a dozen no-fault states, including Florida, Michigan, and New Jersey. In other states it is optional or unavailable.

How does PIP interact with health insurance?

Coordination of benefits determines which coverage pays first, and your health insurer may later seek reimbursement from any settlement you receive. Knowing your state's coordination rules minimizes out-of-pocket costs.

What happens if I miss the treatment deadline in my state?

In Florida, missing the 14-day initial treatment window eliminates your PIP eligibility entirely. Most states have similar windows, so seeking care immediately after any accident protects your access to benefits.

Can PIP run out before all my bills are paid?

Yes. PIP benefits can be exhausted quickly due to policy caps shared across multiple benefit categories. Once PIP is depleted, health insurance, liability claims, and out-of-pocket payments typically cover remaining costs.

Recommended

- How Personal Injury Law Changes 2019 Shape Your Cases | Accident Survival Guide

- Car Accident in Miami, FL: Common Insurance Mistakes to Avoid | Accident Survival Guide

- The Ultimate Charlotte Personal Injury Guide | Accident Survival Guide

- Understanding Your Rights After an Accident (General Education) | Accident Survival Guide