The steps you take in the first minutes and hours after a car accident directly determine the strength of your insurance claim, your legal protection, and your physical recovery. Knowing what to do after a car accident is not optional knowledge. It is the difference between a fair settlement and a costly mistake. This guide covers every critical stage: immediate scene safety, documentation, the car accident claims process, medical evaluation, and your legal rights. Follow these steps in order, and you protect yourself from the most common and expensive post-crash errors.

What are the first steps after a car accident at the scene?

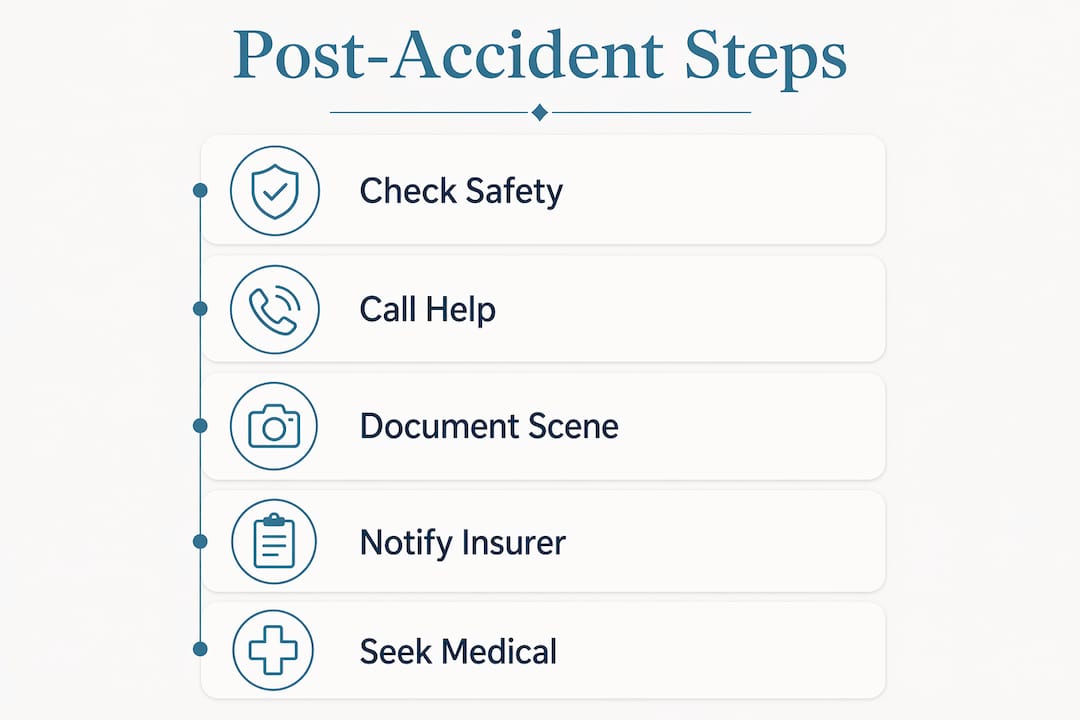

Safety comes before everything else. Before you reach for your phone or exchange information, check yourself and every passenger for injuries. If anyone is hurt, call 911 immediately. Do not move injured people unless there is an immediate danger, such as fire or oncoming traffic.

Once you confirm everyone is safe, move drivable vehicles to the shoulder or a nearby parking lot. Leaving disabled vehicles in active traffic lanes is one of the leading causes of secondary crashes. Activate your hazard lights the moment the collision occurs. If you have reflective triangles or flares in your trunk, place them behind the vehicle to warn approaching drivers.

What information to collect at the scene

Exchange the following with every driver involved:

- Full legal name and contact number

- Driver's license number and state

- License plate number and vehicle make, model, and color

- Insurance company name and policy number

Gather witness contact information separately. Witnesses are independent of both parties, which makes their accounts far more credible to adjusters and attorneys.

Pro Tip: Set your phone camera to embed timestamps and location data in photos before you shoot. This metadata is admissible evidence and can resolve disputes about road conditions, lighting, and vehicle positions.

How to document a car accident properly

Time-stamped photos of vehicle damage, skid marks, traffic signals, weather conditions, and the surrounding road layout are the foundation of any strong claim. Shoot from multiple angles. Photograph every vehicle involved, not just yours. Capture the full intersection or road segment to establish context.

One detail most drivers miss: photograph the other driver's insurance card and license directly rather than copying numbers by hand. Transcription errors on policy numbers delay claims by days.

An official police report is a separate and critical document. Request one even for minor collisions. Officers create an objective record of fault indicators, road conditions, and statements. If police decline to respond to a minor crash, file a self-report through your state's DMV portal within the required window, which varies by state but is typically 10 days.

Do not admit fault, apologize, or speculate about what caused the crash. Stick to observable facts when speaking with officers. A simple "I did not see the other vehicle in time" can be interpreted as an admission of negligence.

How to handle insurance claims and communication with adjusters

Contact your insurer within 24 to 72 hours of the accident. Most policies require prompt notification as a condition of coverage. Delaying this call can give the insurer grounds to complicate or deny your claim. When you call, have your police report number, photos, and the other driver's insurance information ready.

Your insurer will assign a claim number and an adjuster. Write both down immediately. Every future communication should reference your claim number. Keep a written log of every call: date, time, adjuster name, and a summary of what was discussed.

What to submit to support your claim

Strong documentation separates fast, fair settlements from drawn-out disputes. Submit the following as early as possible:

- The police report or self-report filing number

- All scene photos with timestamps

- Witness names and contact information

- Medical records and treatment receipts as they accumulate

- Repair estimates from at least two licensed body shops

- Rental car receipts if applicable

Pro Tip: Never give a recorded statement to the other driver's insurer without first speaking to your own adjuster or an attorney. Recorded statements are used to find inconsistencies, not to help you.

Understanding settlements and total loss thresholds

Keep comprehensive records of all repair estimates, medical bills, and out-of-pocket expenses. Adjusters calculate settlements based on documented losses. Undocumented costs are routinely excluded.

| Stage | What to do |

|---|---|

| Within 24 to 72 hours | Notify your insurer and file the claim with your claim number. |

| Within one week | Submit police report, photos, and initial repair estimates. |

| Ongoing | Track all medical visits, treatments, and related expenses. |

| Before settling | Confirm all injuries are fully diagnosed and repair costs are final. |

Early settlement offers frequently do not account for injuries that develop over days or weeks. Accepting a check before your medical picture is complete closes your claim permanently. Patience at this stage protects your long-term financial recovery.

Why prompt medical evaluation matters even without obvious injuries

Adrenaline is a powerful masking agent. In the immediate aftermath of a crash, your body suppresses pain signals as part of its stress response. Whiplash, soft tissue injuries, concussions, and internal bleeding can all present with zero symptoms for 24 to 72 hours. Seek medical evaluation the same day as the accident, even if you feel completely fine.

Visit an emergency room, urgent care clinic, or your primary care physician. Tell the provider you were in a vehicle collision. This creates a medical record that links your injuries to the accident date, which is the single most important document in any injury claim.

How to build a medical record that supports your claim

Follow every treatment plan your provider prescribes. Missing appointments or stopping physical therapy early creates gaps in your record that insurers use to argue your injuries were not serious. Document the following consistently:

- Every medical visit, including telehealth appointments

- Prescriptions filled and their costs

- Physical therapy sessions and progress notes

- Any emotional or psychological symptoms, including anxiety about driving or sleep disruption

Pro Tip: Keep a daily symptom journal starting the day of the accident. Note pain levels, limitations on daily activities, and emotional impacts. This journal becomes direct evidence of pain and suffering in settlement negotiations.

Independent medical examinations arranged by insurers are a standard part of dispute resolution around injury claims. You may be required to attend one. Bring your own treatment records and be precise about your symptoms. These exams are not neutral. The physician is hired by the insurer.

What legal considerations protect your rights after a crash?

The single most damaging thing most drivers do after a collision is apologize. Saying "I'm sorry" at the scene is treated as an admission of fault in most states, regardless of your intent. Avoid admitting fault to the other driver, to witnesses, and in any communication with insurers. Describe only what you observed.

When the other driver's insurer contacts you directly, you are not obligated to provide a statement immediately. Ask for the request in writing and give yourself time to consult your own insurer or an attorney before responding.

When to consult a personal injury attorney

Legal counsel is recommended in four specific situations: serious or permanent injuries, disputed fault, offers that seem far below your actual losses, and accidents involving commercial vehicles or rideshare drivers. Attorneys who specialize in personal injury work on contingency, meaning you pay nothing unless they recover compensation for you.

For guidance on when hiring a lawyer makes financial sense, review the specific scenarios where legal representation consistently produces higher settlements than self-negotiation.

Keep every piece of evidence organized in a single folder, physical or digital. This includes photos, medical records, repair estimates, correspondence with insurers, and your symptom journal. Organized claimants resolve disputes faster and recover more. Disorganized ones give adjusters room to question the completeness of their losses.

Pro Tip: If the other driver was uninsured or underinsured, notify your own insurer immediately and ask specifically about your UM/UIM coverage. This coverage exists precisely for this situation and is frequently overlooked by accident victims.

Key takeaways

The most effective post-accident strategy combines immediate scene safety, thorough documentation, prompt medical care, and disciplined communication with insurers and legal professionals.

| Point | Details |

|---|---|

| Safety before documentation | Move vehicles, activate hazards, and check for injuries before anything else. |

| Document everything at the scene | Time-stamped photos, witness contacts, and a police report form the core of your claim. |

| Notify your insurer within 72 hours | Delayed notification can give insurers grounds to complicate your coverage. |

| Get medical care the same day | Adrenaline masks injuries; a same-day medical record links your injuries to the accident date. |

| Never accept early settlements | Wait until all injuries are diagnosed and repair costs are confirmed before signing anything. |

What I've learned from navigating accidents firsthand

Most people walk away from a crash thinking the hard part is over. It is not. The hard part is everything that comes next, and most people are completely unprepared for it.

When Kathy and I went through our own accidents, the thing that hurt us most was not the crash itself. It was not knowing what to say, what to sign, and what to hold back. Insurers move fast. They call within hours. They sound helpful. They are not working in your interest. That is not cynicism. It is how the system is built.

The detail I wish someone had told me: your first 24 hours after the crash set the trajectory for everything else. The photos you take, the statements you give, the medical appointment you keep or skip. Every one of those decisions has downstream consequences that are very hard to reverse.

I also see people consistently underestimate delayed injuries. They feel fine, they skip the doctor, and three weeks later they are in serious pain with no medical record connecting it to the accident. That gap costs them real money and real health outcomes.

Stay calm, stay factual, and document more than you think you need to. You can always discard evidence you do not need. You cannot create evidence after the fact.

— Scott

How Accidentsurvivalguide can help you right now

Knowing the steps is one thing. Applying them under stress, with an adjuster calling and a car in the shop, is another challenge entirely.

Accidentsurvivalguide provides free, plain-language resources built specifically for people in your position. Use the free compensation calculator to get a realistic estimate of what your claim may be worth before you speak with any adjuster. If you are in a specific state, check the dedicated guides for Virginia accident steps and Massachusetts requirements to make sure you meet local deadlines and legal obligations. Every resource on the site is free, and the goal is simple: help you make informed decisions before you sign anything.

FAQ

What should I do immediately after a car accident?

Check for injuries, call 911 if needed, move vehicles to safety, activate hazard lights, and exchange insurance and driver information with all parties involved. Document the scene with time-stamped photos before leaving.

Do I have to call the police after a minor accident?

Most states require a police report when there is injury, death, or property damage above a set dollar threshold, typically between $500 and $1,000. When in doubt, call. An official report strengthens your claim and reduces fault disputes later.

How long do I have to file an insurance claim after an accident?

Most insurers require notification within 24 to 72 hours, though policy terms vary. State statutes of limitations for personal injury lawsuits typically range from one to three years, depending on the state.

Should I accept the first settlement offer from the insurance company?

No. Early settlement offers frequently do not reflect the full cost of injuries that develop over days or weeks. Wait until your medical treatment is complete and all repair costs are confirmed before accepting any offer.

When should I hire a personal injury attorney after a crash?

Consult an attorney if you have serious injuries, disputed fault, a commercial vehicle was involved, or the initial settlement offer seems far below your actual losses. Most personal injury attorneys work on contingency and charge nothing unless they win your case.